Relief from Stamp Duty Land Tax (SDLT) for purchases of multiple dwellings will be abolished, following The Chancellor, Jeremy Hunt’s announcement in the Spring Statement last month.

Also known as Multiple Dwellings Relief (MDR), it can benefit purchases of two or more residential properties in single or linked transactions.

We’ve asked Matt Orange, Head of Indirect Tax, to outline MDR in more detail, and to highlight the upcoming changes.

Over to Matt

Originally introduced in 2011, MDR was intended on boosting demand for residential properties and the private rented sector housing supply.

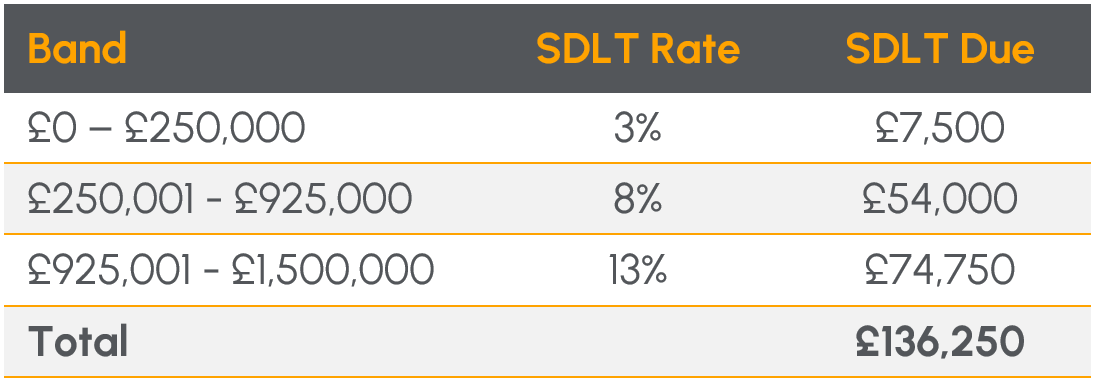

When two or more residential properties are purchased in a single or linked transaction, Stamp Duty Land Tax (SDLT) is payable on the total price paid for all properties.

For example if an individual purchased three residential properties from the same developer, two of which cost £550,000 and the other £400,000 (total £1.5m), SDLT is calculated as follows:

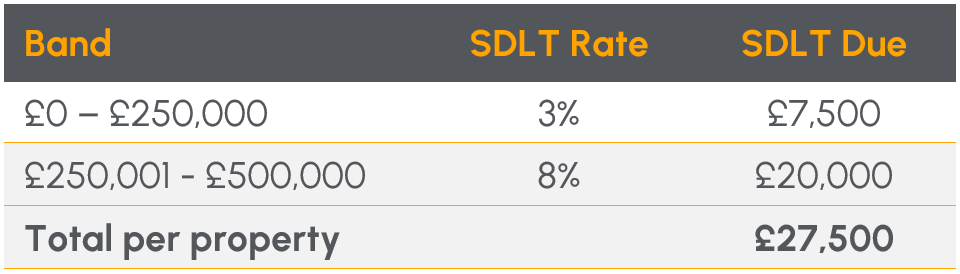

To work out the SDLT payable with an MDR claim, we take the average price of each property and calculate the SDLT payable using that figure.

Average price = £1,500,000 / 3 = £500,000

Next we multiply the £27,500 by the number of properties purchased to arrive at the total SDLT payable.

Total SDLT payable with MDR £27,500 x 3 = £82,500.

So we can see MDR has achieved a considerable SDLT saving of £53,750 (£136,250 – £82,500).*

Between 2022 and 2023 HMRC estimate MDR cost £700m and found no strong evidence that the relief was meeting its original objectives. Furthermore, HMRC believe the relief is subject to abuse with many spurious claims appearing before tax tribunals.

Relief can still be claimed on transactions that substantially perform before 1 June 2024, or in cases where contracts were exchanged on or before the 6 March 2024, even if completion of the purchase is on or after 1 June 2024.

Non-residential rates will continue to apply to acquisitions of 6 or more residential properties.

*SDLT legislation is complex and assumptions have been made in arriving at these figures so this should not be taken as advice. Calculations are based on rates applicable on the 7 March 2024.

Here to help

If you are looking for advice about the abolishment of multiple dwellings relief, our expert team are here to help. Please fill out the form below and one of our advisers will be in touch.