A question our specialist property team get asked a lot is “what is a spotlight?”. To put it simply, a “Spotlight” identifies schemes that HMRC believes do not work – think of it acting as a warning.

In the realm of property business arrangements, a notable cautionary signal also exists called Spotlight 63, recently highlighted by HMRC. This spotlight illuminates schemes deemed ineffective and serves as a stark warning for those involved in such practices.

We’ve asked Jonathan Jones, Senior Client Manager, to shed some light into the implications of engaging business arrangements that involve hybrid partnerships.

Over to Jonathan

If you’re thinking of a property business arrangement, and want to use a scheme, HMRC will:

- open an enquiry into your tax affairs

- seek full payment of any tax due, plus interest

- charge higher penalties where appropriate

What is a Spotlight 63?

HMRC have issued Spotlight 63 on property business arrangements involving hybrid partnerships.

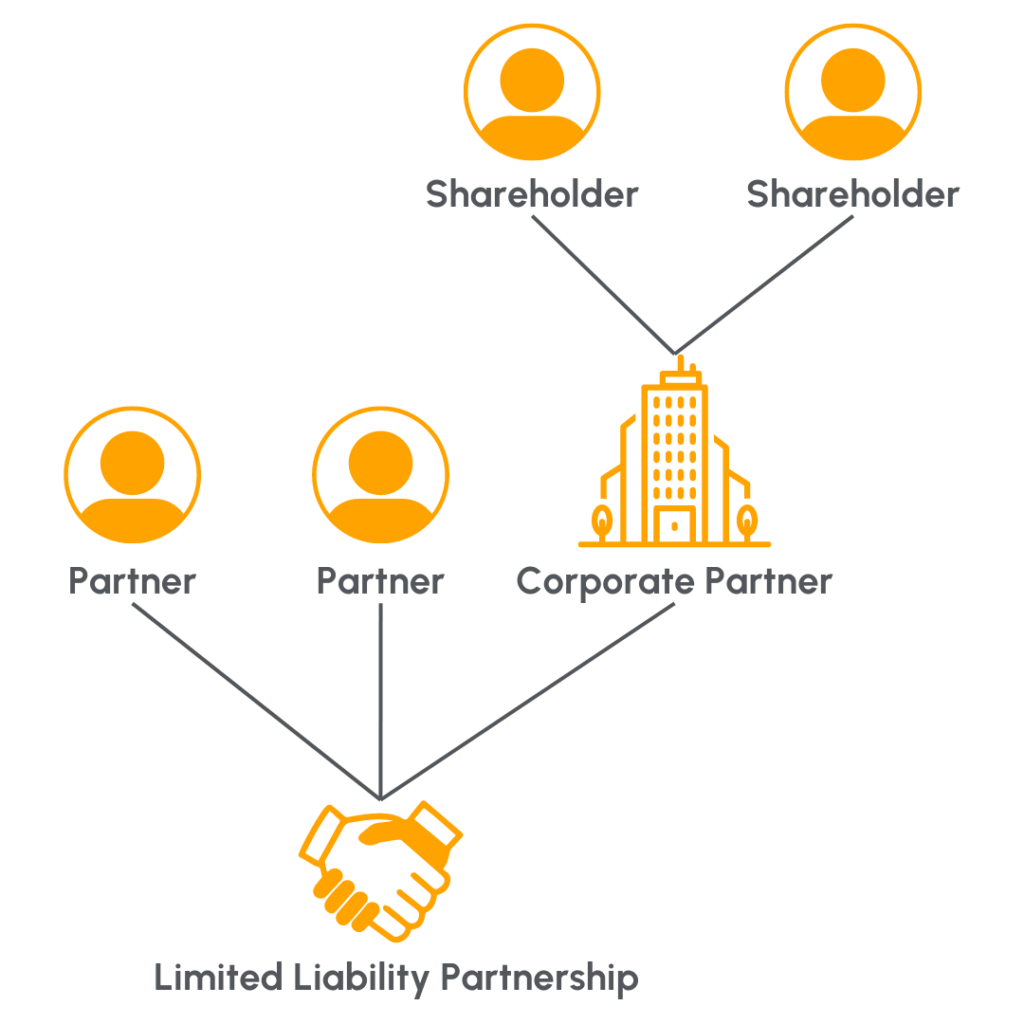

HMRC contends that the arrangements seek to avoid tax by allowing individual or joint property landlords to transfer their properties to a limited liability partnership (LLP) with a corporate partner. The below diagram helps to explain:

The arrangements claim to work as follows:

- The individual landlords or their family members, or both, set up a limited company.

- The individual landlords set up an LLP alongside the limited company – the limited company is considered the corporate partner.

- The individual landlords transfer their properties to the LLP.

- The partners of the LLP (the individual partners and corporate partners) allocate the LLP profits to themselves on a discretionary basis to make sure that:

a) The individual partners remain basic rate taxpayers

b) The remaining profits are allocated to the corporate partner. - The corporate partner claims a deduction for finance costs (such as mortgage interest) relating to the properties.

What are the promotors claimed benefits?

Landlords are advised by promotors that this arrangement results in less tax for the following reasons:

- The transaction relating to the contribution of properties to the LLP has no upfront tax cost and properties’ base costs are uplifted to their market value at the date of transfer for Capital Gains Tax;

- The landlords remain basic rate taxpayers meaning they are not impacted by finance cost restrictions;

- The corporate member is subject to Corporation Tax on its net profit share instead of paying higher or additional income tax rates that would apply if the profits had been allocated to the landlords;

- Calculating the capital gain using an uplifted base cost at the date the properties are contributed to the LLP reduces the Capital Gains Tax paid compared to using the original purchase and improvement costs, if the property is sold;

- Business Property Relief may be claimed in respect of a hybrid structure carrying on a property rental business resulting in no Inheritance Tax being due, if the landlord dies.

Do property business arrangements involving hybrid partnerships work?

HMRC’s believe that this scheme does not work. HMRC provide a long list of reasons why this scheme does not work.

In my view, it is difficult to disagree with HMRC’s technical analysis.

What should you do if you are using this arrangement?

If you are already involved in this arrangement and want to get out, HMRC strongly advises you to withdraw from it and settle your tax affairs as soon as possible.

Restriction on mortgage interest and other schemes

The property business arrangement involving hybrid partnerships originally sought to address issues where an individual higher rate landlord suffers a restriction on mortgage interest tax relief.

It is possible to incorporate a property portfolio to overcome the restriction on mortgage interest tax relief. Nevertheless, this can only be carried out in the right circumstances without any draconian tax charges.

There are many other schemes out in the market which are also subject to some debate as to their effectiveness. I am particularly concerned with the incorporation of property portfolios that are carried out without notifying the mortgage lender.

Here to help

If you’re wanting to explore your options for a property business arrangement with a hybrid partnership, we are here to help. To speak to our expert team of property specialist accountants, please fill out the form below.