As the UK economy grapples with the repercussions of recent financial policies, landlords find themselves facing significant challenges. The Bank of England’s decision to keep interest base rates at 5.25%—a dramatic increase from the 0.10% seen in March 2020—has had profound implications for property investors.

Jonathan Jones, Senior Client Manager and Property Specialist, has outlined the most recent interest rates and the impact this has on individual and company landlords.

Take it away Jonathan

The Bank of England has continued to keep interest base rates frozen at 5.25%. This is a mammoth increase for landlords when compared to the interest base rates of 0.10% in March 2020.

It means landlords will face higher finance costs (mortgage interest) and a reduction in their after-tax returns on property investments.

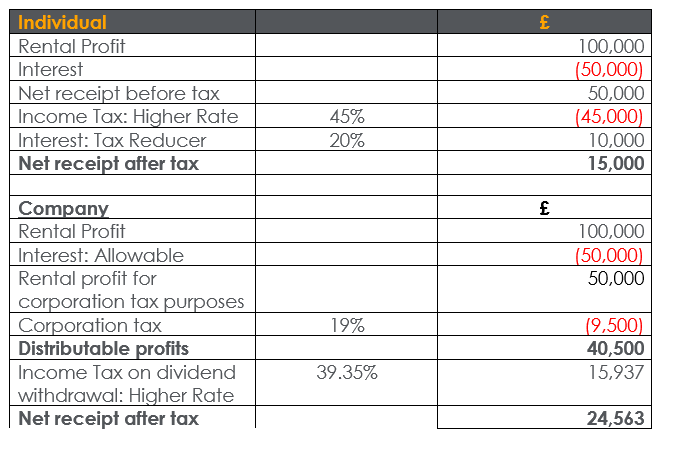

Individual Landlords

Individual landlords are not able to deduct all of their finance costs from their rental income to arrive at their rental profits. Instead, they receive a basic rate reduction from their income tax liability for their finance costs.

Higher finance costs are likely to result in higher tax liabilities due to:

- Income tax rates – The non-deductibility of interest costs may cause the individual to become a higher rate or additional rate taxpayer.

- Abatement of personal allowance – The non-deductibility of interest costs may cause the individuals taxable income to exceeds £100,000. Consequently, their personal allowance will be abatement and they will suffer a 60% marginal rate of tax as the personal allowance is withdrawn.

- Higher income child benefit charge – The non-deductibility of interest costs may cause adjusted net income to exceed £60,000 so that child benefit will be progressively withdrawn.

Company Landlords

There is no restriction of finance costs for companies (i.e. mortgage interest is deductible). Landlords are likely to benefit from holding property in a company where:

- Rental profits are taxed at the higher or additional rate of income tax.

- The property is subject to a mortgage.

- Not all after-tax funds are needed by the property business owner.

Comparison

The following calculations show net receipts after-tax of:

- £15,000 for an individual landlord subject to additional rate tax.

- £24,563 for a company where all profits are withdrawn.

- £40,500 for a company where all profits are retained (say for further investment).

A saving of between £9,563 and £25,500 per annum by holding property in a company.

Incorporation of a Property Portfolio

The incorporation of a property portfolio will have Capital Gains Tax and Stamp Duty Land Tax implications. Nevertheless, Capital Gains Tax and/or Stamp Duty Land Tax may be avoided or mitigated in the right circumstances.

Call To Action

A landlord needs to identify and understand how rising interest rates affects their tax position. Only then will they be able to take the necessary steps, such as the incorporation of a property portfolio, to ensure they maintain a viable property portfolio.

Here to help

If you’re a landlord and are looking for advice about the latest interest rates or how to hold property (individual, partnership, company), we’re here to help. To speak to one of our property experts, please fill out the form below and we’ll be in touch shortly.