New allowances such as the super deduction as well as changes to the existing capital allowances regime have been introduced in recent years.

Full Expensing (FE) is a new capital allowance that was introduced in 2023 and made permanent in the 2023 Autumn Statement. It’s a 100% first-year allowance, which in other words, means that companies can claim a deduction from taxable profits that is equal to 100% of their qualifying expenditure in the year that expenditure is incurred.

Although this was a welcomed allowance, there are pitfalls to avoid when it comes to full expensing. We’ve asked Christine Wise, Tax Manager from our Manchester office, to explain more.

Over to Christine

Full Expensing was brought in to replace the super-deduction which ended in March 2023. The super-deduction was seen as a temporary measure to encourage businesses to invest in capital assets but not to delay expenditure until April 2023 when the new higher tax rate kicked in- a post-covid economic kick start.

Full Expensing- What’s really covered

Full Expensing is not available to Partnerships, sole traders or LLPs. It’s only available to Companies.

It’s worth noting however that most businesses who are not eligible, can still claim Annual Investment Allowance (AIA), which offers a similar benefit on the expenditure of up to £1 million per annum.

Full Expensing (FE) allows companies to write off the cost of capital assets in full in the year of acquisition. Of course, as with all first-year allowances, there are some limitations; the allowance only applies to plant and machinery which is new. So, no second-hand assets are covered. This is also a restriction on purchases from a connected party unless the asset is unused and the sale or manufacture is part of the seller’s trade and acquired under normal terms.

Qualifying types of equipment for Full Expensing include:

- Warehousing equipment such as forklift trucks

- Tools such as ladders and drills

- Construction equipment such as bulldozers and excavators

- Machines such as computers and printers

- Vehicles such as tractors

- Lorries and vans

- Office equipment such as chairs and desks

- Some fixtures such as kitchen and bathroom fittings

- Fire alarm and security systems

Additionally, assets acquired by a business for onward leasing to others are not generally eligible for FE.

How does it work and how is it different to AIA

So, now we’ve gone through what’s covered, how does it actually work in practice?

AIA has an upper limit of £1M which is split where there is more than one company under control of the same person(s). This can be problematic where the companies are not within a group and another company has made a significant AIA claim.

In comparison there is no ceiling to the value of qualifying assets where FE may be claimed. Of course, assets must be for use in the business and must not be for a contrived or uncommercial purpose.

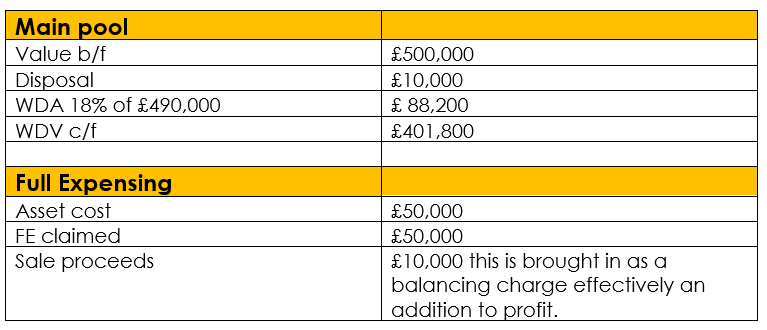

The FE assets form a separate pool, this is important because the treatment of assets on disposal is different to those in the main pool.

Each asset in the FE pool is recognised separately, and a balancing charge is brought in in full.

As an example:

Whereas within the AIA main pool the reduction in allowances claimed is £1,800. A balancing charge only applies to the main pool where all assets have been disposed. In this example let’s assume the asset sold has had AIA claimed against it, but other assets are held within the pool.

So, where a company has a main pool value at the start of its accounting period, it would be preferable to claim AIA over FE.

Another potential pitfall is that if you maximise your company capital allowance claims and create a loss, only 50% of the amount over £5M may be carried forward. Consequently, it make may more sense to only claim the 18% WDA in the year of purchase and a higher WDA in later years than forgo any losses.

Finally the write off of asset cost in full for tax creates a deferred tax liability on the company balance sheet as the tax relief exceeds the depreciation charged in the accounts.

Here to help

If you have any questions on full expensing, or are looking for advice on the matter, we’re here to help. To speak to one of our tax experts, please fill out the form below and we’ll be in touch.