The Annual Reconciliation Report (ARR) process for the 2023-24 financial year opened on Compass on 1st April 2024. The ARR needs to be completed by 30th June 2024 and is a contractual obligation for all dentists who have performed on an NHS contract in the year.

The ARR is the process of submitting all dentists net pensionable earnings (NPE), or net pensionable earnings equivalent (NPEE), if the dentist is not a member of the NHS pension scheme. The NPE finalises the pension contributions due for the year for the dentist. This is compared to the actual contributions made in the year, with an adjustment made on the July NHS schedule for any under or overpayment made by the dentist.

We’ve asked Tom Slevin, Dental Client Services Director, to explain the process.

Take it away Tom…

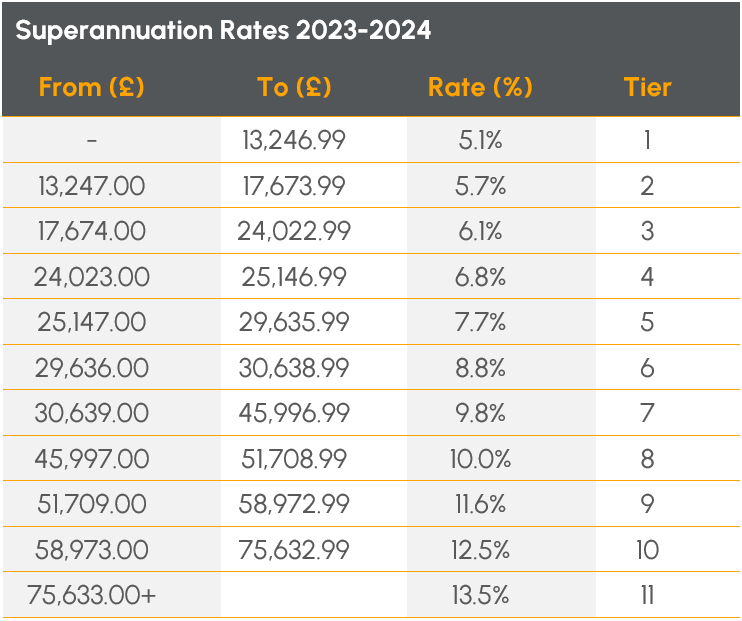

In the 2022-23 contract year, we had changes to the NHS pension scheme rates and tiers half way through the year, which made the calculation of the pension contributions due in the year more difficult than normal. Thankfully in 2023-24, there was only one set of pension contribution tiers for the year (although even some of the thresholds for the bands were updated during the year in line with NHS Pension regulations).

The pension contribution tiers for the year were as follows:

NPE calculation

A dentists NPE is calculated as their net NHS earnings for the year. For an associate dentist, this is the income the associate receives for the NHS treatments they have carried out – income for UDAs less NHS labs, hygienist charges, levies and any other NHS costs the practice may deduct from their pay.

Although the calculation appears straightforward, this isn’t always the case. We see many weird and wonderful pay schedules from associate dentists, with many not splitting out the laboratory bills for NHS patients and private patients for example. If these haven’t been split out, then the NPE cannot be calculated accurately. In most cases, a pragmatic view needs to be taken on how these laboratory bills should be split when calculating NPE. We also commonly see dentists ask us why the dental practice has calculated their NPE as 43.9% of their gross income paid for NHS work.

This is a common misconception and relates to the pensionable ceiling for the NHS contracts. The pensionable ceiling for a NHS contract sets the maximum NPE/NPEEs for all performers on the contract for the year and the total cannot exceed 43.9% of the contract value. Some dental practices historically have then applied the 43.9% to the gross income paid to the associate (the NHS income before lab bills, license fee and other costs). However, in our experience, this usually results in a lower NPE figure for the associate than working out the actual NPE correctly.

When the NPE is calculated, this should be entered onto Compass by the practice or the associate and both parties should agree this figure on Compass by 30 June 2024.

We can help

Our team of experts have extensive experience in helping both dental practices and associate dentists with their Annual Reconciliation Report requirements, as well as being able to advise on NHS pension issues associated with this. If you need assistance with this or any other dental financial matter, give us a call on 0151 348 8400 or email [email protected].