Big changes are in place for R&D Tax Reliefs with the launch of a new Merged Scheme for companies with accounting periods beginning on or after 1 April 2024.

Overview of the Merged Scheme

The aim of the New Merged RDEC (R&D Expenditure Credit) scheme, also known as the R&D single scheme or simplified scheme, is to provide simplification, consistency and effectiveness for R&D reliefs by combining the previous SME and RDEC (for large businesses) schemes into a single structure.

If your company currently claims under the SME or RDEC regime then from its next accounting period beginning on or after 1 April 2024 the new Merged Scheme will most likely apply.

New Merged RDEC Scheme

The Merged Scheme adopts the RDEC payment model, offering an above-the-line expenditure credit at a rate of 20% (gross).

Extra Relief for R&D-Intensive Businesses

In addition to the new Merged Scheme, there is also a separate Enhanced R&D Intensive Support (ERIS) scheme specifically for loss-making R&D-intensive SME businesses. This offers the previous SME tax credit rate of 14.5%. To qualify for ERIS, at least 30% of a company’s total expenditure must be related to R&D.

New Rates for R&D Tax Reliefs

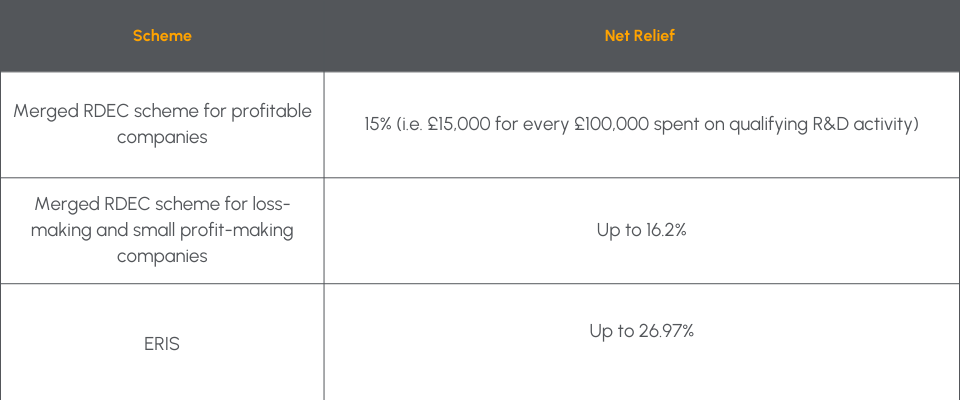

The new schemes offer different levels of benefit for every £1 spent on qualifying R&D activity, summarised in the table below:

Other new points to consider

Contracted Out R&D and Subcontractor Costs

As part of these overall changes, new rules are also being introduced for contracted out R&D, subcontractor R&D costs, subsidised expenditure and overseas R&D expenditure.

Does it change what qualifies as an R&D Project?

The criteria for what constitute a qualifying project for R&D Tax Reliefs under the Merged RDEC scheme remain largely unchanged, with any project still needing to meet the following conditions:

- There must be scientific or technological uncertainty.

- The project must aim to achieve an advance in overall knowledge or capability in a field of science or technology.

- That advance must not be readily deducible by a competent professional in the field.

What does our R&D Incentives Director, Tom Whitworth think?

“The new Merged RDEC scheme undoubtedly represents a significant shift in the landscape of R&D Tax Reliefs. By combining the SME and RDEC schemes, the government aims to simplify the process, making it more consistent and accessible for businesses of all sizes.

On similar lines, the Enhanced R&D Intensive Support (ERIS) scheme is a particularly welcomed addition. It acknowledges the crucial role that R&D-intensive SMEs play in driving innovation. This could be a game-changer for these businesses, providing them with the necessary support to continue their ground-breaking R&D work.

Overall, the changes present new requirements for businesses to ensure that their R&D Tax Reliefs claims are correct and compliant.”

If you would like to discuss the changes with Tom, or one of our R&D Incentives team, please get in touch and we’d be happy to help.