Whilst Employee Ownership Trusts (EOTs) have been around since 2014, the concept has seen a boom in the last few years, with over 1,000 companies in the UK now using this model.

It’s not just small companies that are embracing this structuring option either; key household names, like the John Lewis Partnership and Aardman Animations have adopted an EOT structure that promotes employee governance and ownership, and with it comes a variety of tax and commercial benefits too.

Why are EOTs so sought after by companies? Why have they become a key exit planning tool? What requirements must be met to qualify for one? I’ve ran through all the questions I get when discussing EOTs with people for the first time. Let’s delve into the details.

What is an Employee Ownership Trust?

In a nutshell, employee ownership describes a business which is fully or partially owned by its employees.

You’ll likely consider an EOT when your company/group is considering corporate restructuring, succession planning or shareholder exits.

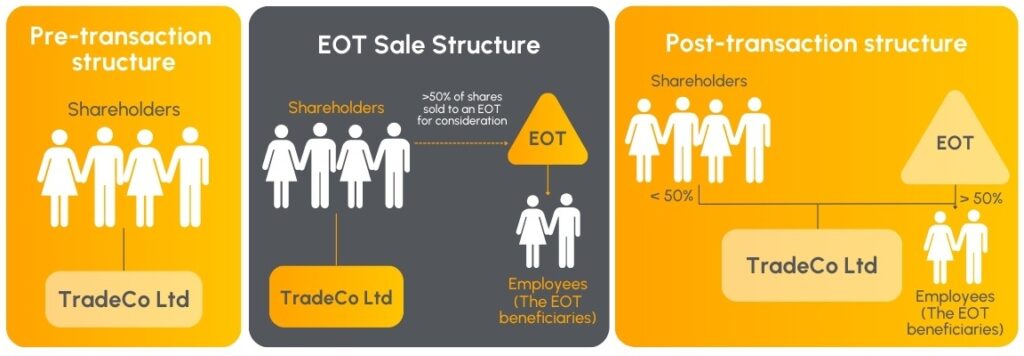

The nature of an EOT is specifically hinted at in its name. The employees do not hold shares in the business directly, but instead, a trust acts as the independent legal entity that acquires shares in the company/group on behalf of all eligible employees from the existing shareholders. The below illustrations demonstrate the basic mechanics of a share sale to an EOT:

The aim of an EOT then is to strengthen employee engagement by having them accountable and involved in the business’ future plans and opportunities, whilst allowing all staff to potentially benefit financially from the success of the company.

Who are the key people involved in an Employee Ownership Trust?

The EOT itself is managed by the Trustee Board, which typically comprises of a combination of:

- Existing company directors;

- Independent trustees, and;

- Employee representatives.

All who must act in the best interests of the EOT’s beneficiaries. The group/company’s eligible employees will effectively be such beneficiaries.

What are the benefits of an EOT?

Provided a number of conditions are met (see later on), there are numerous tax and commercial benefits, not only for the selling shareholders but for the employees too.

For the selling shareholders

One of the main benefits for the sellers is when they dispose of their shares to an EOT, they are exempt from Capital Gains Tax (CGT).

This has become even more significant due to the changes outlined in the Autumn Budget, which saw the reduced rate of CGT under Business Asset Disposal Relief (BADR) grow from 10% to 14% in April 2025, and increasing again to 18% in April 2026.

As a result, if we compare EOT sales to alternatives such as trade sales or management buyouts (MBOs), the savings on CGT can make this an incredibly attractive option to business owners.

To put this into a real world example, the sale of shares held by a husband and wife, worth a market value of £10m (originally subscribed for nominal value of £1 per share) could generate a combined CGT saving of over £2,000,000 (based on 2024/25 CGT and BADR rates).

A secondary benefit is that the sale to an EOT is seen as a much simpler and quicker sales route than its alternatives. This is because the sellers effectively also ‘act as the buyers’ and therefore extensive due diligence work and offer negotiation rounds aren’t required.

Other benefits include no ‘minimum’ share ownership/share ownership period requirement for the sellers, and shareholder-directors can also partake in the Income Tax-free bonuses in the same way as eligible employees can (see below).

For the employees

It’s not just shareholders that will feel the benefit though, eligible employees can receive Income Tax-free bonuses of up to £3,600 per tax year!

Existing discretionary bonus schemes are still available and may continue to be utilised in conjunction with EOT bonuses. Of course, these bonus schemes would still be subject to Income Tax and National Insurance as usual.

Employees also have the peace of mind that any future sale of the company would have to be deemed in the employees’ best interests, with all eligible employees sharing equitably in the proceeds of the sale.

Importantly, the employees’ day-to-day responsibilities will not be disrupted as a consequence of the EOT sale; there will simply be a change in the overall business structure that provides additional benefits to them.

What are the qualifying conditions?

The benefits make it clear why EOTs are so popular, but to qualify for an EOT you must meet a number of detailed requirements. I have summarised the main ones below:

- The trading requirement – The company being sold must be a trading company or the holding company of a trading group.

- The all-employee benefit requirement – All employees should be eligible to benefit from the EOT, subject to a qualifying employment period of up to one year (but can be less if specified in the EOT documents).

- The equality requirement – All employees must be able to benefit on the same terms.

- The controlling interest requirement – Before the tax year in which the EOT acquires the shares, it must:

- Not hold a controlling interest in the company (i.e. controlling interest is typically >50% of the total shares in the company, but does include other meanings),

- Acquire a controlling interest in the company during the EOT sale, and;

- Continue to hold it for the remainder of the tax year of sale.

- The limited participation requirement – The number of employees who own more than 5% of the income or capital of the company being disposed of, together with any relatives who are also employees of the company/group, must not exceed 40% of total employees.

A breach of any of these conditions (known as a disqualifying event) could ultimately lead to a claw-back of the CGT exemption granted to the sellers, or, if enough time has passed, the CGT that should have been paid upon sale will instead become payable by the trust. It can also mean that the Income Tax-free benefits for any bonuses awarded to employees will be revoked.

Is an EOT right for you?

To help you decide if an EOT could be the right move for your business, take a look at how we recently supported our client’s business growth journey by helping them to become an EOT.

Speak to our specialist team of advisers who are on-hand to answer any questions you might have about EOT’s and guide you every step of the way.